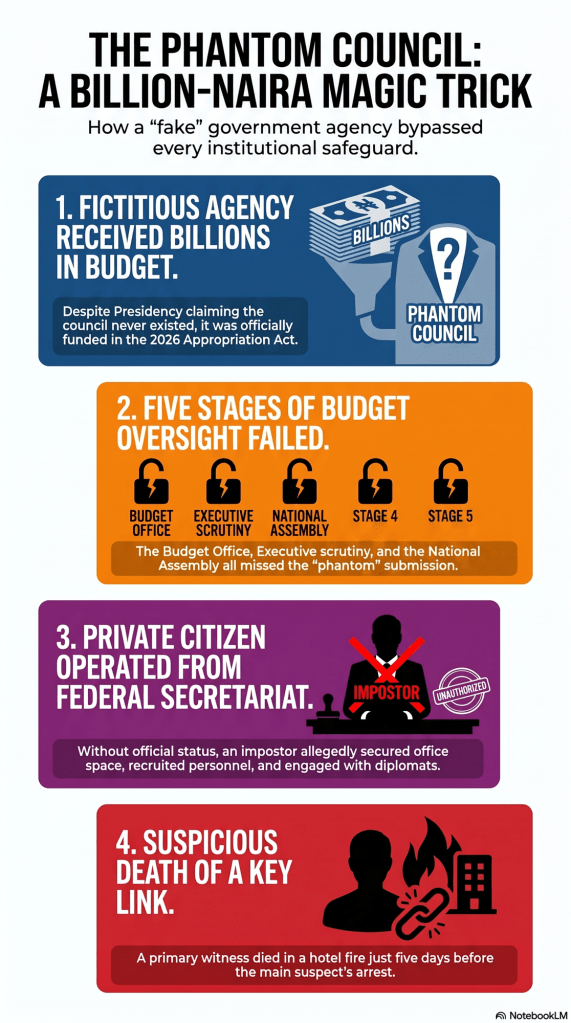

Nigeria’s budget oversight mechanisms form a critical pillar of public financial management (PFM) in Africa’s largest economy. Governed primarily by the 1999 Constitution (as amended), the Fiscal Responsibility Act (FRA) 2007, and supporting frameworks, these mechanisms aim to ensure fiscal discipline, transparency, accountability, and alignment of public spending with national priorities. However, persistent challenges — including budget padding, ghost projects, weak enforcement, and low public participation — reveal significant gaps, as highlighted by recent controversies like the alleged phantom Presidential Council in the 2026 Appropriation Act.31

1. Legal and Institutional Framework

The Constitution vests the National Assembly with the “power of the purse” (Sections 80–81). No money can be withdrawn from the Consolidated Revenue Fund without appropriation. Key institutions include:

- Executive Side:

- Budget Office of the Federation (BOF): Coordinates preparation, monitors implementation, and issues quarterly reports under FRA Section 30/50.

- Ministry of Finance, Budget and National Planning: Leads policy and Medium-Term Expenditure Framework (MTEF).

- Fiscal Responsibility Commission (FRC): Enforces fiscal rules.

- Office of the Auditor-General for the Federation (OAuGF): Conducts post-expenditure audits (Section 85, Constitution).

- Legislative Side:

- National Assembly (Senate and House): Approves budgets via Joint Committees on Finance and Appropriations; conducts oversight through sector committees.

- Public Accounts Committees (PACs): Review Auditor-General reports.

- Other Actors: Civil society (e.g., BudgIT), media, and citizens via participatory mechanisms.

Medium-Term Expenditure Framework (MTEF) and Fiscal Strategy Paper (FSP) provide a multi-year anchor, requiring National Assembly approval.21

2. Stages of the Budget Cycle and Oversight Points

Oversight operates across four main phases:

a. Preparation and Formulation (Executive-led)

MDAs submit estimates guided by MTEF/FSP. BOF collates and FEC approves. Limited early legislative or public input occurs, though FRA mandates some consultation.

Oversight here: Weak in practice; relies on internal executive checks.

b. Authorization/Approval (Legislative)

President presents the Appropriation Bill. National Assembly scrutinizes, holds public hearings (in theory), amends, and passes it. This is where “budget padding” often occurs — lawmakers inserting constituency or unverified projects.42

Nuance: Nigeria operates a “budget-making legislature” model, unlike pure Westminster systems where legislatures mainly amend marginally. This grants significant power but invites abuse.

c. Implementation and Monitoring (Ongoing)

BOF and MDAs execute. FRA requires quarterly performance reports to National Assembly and FRC. Sector committees conduct site visits and summons.

Challenges: Delayed or non-publication of Budget Implementation Reports (BIRs); virement (fund reallocation) without adequate approval; revenue shortfalls leading to supplementary budgets.

d. Audit and Evaluation (Post-Expenditure)

OAuGF audits accounts and submits to National Assembly. PAC reviews and recommends sanctions.

Edge Case: Audits often delayed (sometimes years), reducing timeliness. Limited follow-up on queries means little prosecution.

3. Performance Assessment

International benchmarks like the Open Budget Survey (International Budget Partnership) consistently rate Nigeria poorly:

- 2023 scores: Transparency ~31/100, Oversight ~61/100, Public Participation ~19/100 (decline from prior years).2

- Strengths: Some online portals (Open Treasury Portal) and civil society tracking (BudgIT).

- Weaknesses: Budget treated as semi-secret; vague line items; poor citizen access.

Real-World Examples and Scandals:

- Budget Padding: Recurrent issue — e.g., alleged ₦6.9 trillion inserted by National Assembly in 2025 without justification (BudgIT report). Projects like inflated boreholes or duplicated items.42

- 2026 Phantom Council: Alleged allocation of ~₦1.3 billion to a disputed Presidential Foreign Intervention Promotion Council/Economic Advisory Council in the signed Appropriation Act, despite Presidency denial. This exposes failures in verification during drafting, review, and approval stages — raising questions about who inserted/approved the line and why safeguards missed it.31

- Historical cases: Padding scandals in 2016 (₦40bn+), repeated under multiple administrations.

These illustrate how oversight can fail at multiple choke points: poor documentation trails, political interference, capacity gaps, and weak enforcement.

4. Nuances, Edge Cases, and Systemic Implications

- Political Economy: Budgets are tools for patronage. Constituency projects often blur lines between oversight and self-interest. Executive-legislative tensions (e.g., delayed passage) exacerbate issues.

- Federalism: State and local budgets have parallel (often weaker) mechanisms, compounding national challenges.

- Digital and Civil Society Role: Tools like BudgIT’s trackers improve transparency, but government resistance limits impact. Open Government Partnership commitments for participatory budgeting remain partially implemented.

- Corruption Risks: Weak oversight enables ghost workers, abandoned projects, and extra-budgetary spending. Debt servicing crowds out capital expenditure.

- Reform Efforts: FRA 2007, ongoing PFM reforms, and calls for full implementation of International Public Sector Accounting Standards (IPSAS). Yet enforcement lags.

- Edge Cases: Emergency/supplementary budgets (e.g., COVID or fuel subsidy removal) often bypass rigorous scrutiny. Security votes remain opaque.

Implications:

- Economic: Distorted priorities, inefficiency, and fiscal unsustainability (high debt service).

- Social: Undermines service delivery (health, education, infrastructure) and public trust.

- Governance: Erodes democratic accountability; fuels cynicism and instability.

- International: Affects investor confidence and aid effectiveness.

5. Recommendations for Strengthening Mechanisms

- Enhance Transparency: Mandate timely, machine-readable publication of all budget documents, virements, and audits. Full Open Treasury Portal functionality.

- Bolster Legislative Capacity: Independent budget research office (like Nigeria’s NILDS but strengthened); mandatory public hearings with CSO input.

- Enforcement: Automatic sanctions for padding or unverified lines; empower FRC and OAuGF with more independence and resources.

- Technology and Participation: Real-time citizen monitoring platforms; integrate participatory budgeting from MTEF stage.

- Post-Audit Follow-Up: Binding timelines for PAC recommendations and prosecutions.

- Cultural/Political: Bipartisan reform and political will to treat budget as public good, not spoils system.

In the context of the 2026 phantom council saga, these mechanisms highlight a core tension: formal structures exist, but their effectiveness depends on political commitment, technical capacity, and societal vigilance. Without addressing root causes — weak institutions, corruption incentives, and opacity — Nigeria’s budgeting will continue to fall short of its developmental potential.7

Comprehensive reform requires coordinated action across branches of government and active citizenship. Progress is possible, as seen in incremental improvements in some reporting, but sustained political will remains the decisive factor.